Webinar: How AI Agents Are Transforming Sales Compensation Management | Wednesday, July 22

Register

- An accrued commission is a commission expense earned by sales staff in a reporting period but unpaid at period-end; under accrual accounting it’s recognized when earned and recorded as a current liability (e.g., "Accrued Commissions" or "Commissions Payable").

- Recognition requires a clearly defined trigger in the commission plan (examples: contract signature, customer invoice, first payment, or delivery); record the accrual in the period the trigger is met to satisfy the matching principle.

- Typical journal flow: at period-end debit Commission Expense / credit Accrued Commission Liability; on payout debit Accrued Commission Liability / credit Cash (or Payroll Payable); reverse or adjust for clawbacks or cancellations.

- Normative treatment: ASC 606 (US GAAP) and IFRS 15 may require capitalization of incremental contract acquisition costs (commissions) and systematic amortization over the contract/customer life rather than immediate expensing—assess per contract and policy.

- Practical best practices: choose an accrual method that fits your plan (flat %, tiers, multi-variable), reconcile accruals to payroll and CRM data, implement internal controls and automation (commission software) to ensure accuracy, auditability and timely month‑end close.

How can you get an accurate picture of your company's financial health if your expenses aren't recorded in the same period as the sales that generated them? This is a common challenge for businesses with commissioned sales teams. The solution lies in understanding and correctly accounting for accrued commissions. This isn't just a bookkeeping task; it's a fundamental practice that impacts your financial statements, sales team motivation, and overall business strategy.

Accrued commissions represent the compensation your sales team has earned but has not yet been paid. By recording these as they are earned, rather than when the cash leaves your account, you ensure your financial reports are accurate, transparent, and compliant with key accounting principles. This guide will walk you through the definition, accounting treatment, and best practices for managing commission accruals effectively.

What Exactly Is an Accrued Commission?

An accrued commission is an expense that a company has incurred for sales generated within a specific accounting period, but the payment for which will be made in a future period. It is recorded on the company's balance sheet as a current liability, often under "Accrued Liabilities" or "Commissions Payable."

This practice is rooted in the accrual basis of accounting, which stands in contrast to cash-basis accounting.

Accrual vs. Cash Accounting

Under the accrual method, revenues and expenses are recognized when they are earned or incurred, regardless of when the cash transaction occurs. This provides a more accurate representation of a company's performance by matching expenses to the revenues they helped generate (the "matching principle"). Cash accounting, on the other hand, only records transactions when cash is exchanged, which can distort the financial picture of a given period.

For sales commissions, this means the expense should be recognized in the month the sale was made, not the month the salesperson receives their payout.

Key Components of Commission Accruals

To properly calculate and record these liabilities, you need to understand their core components:

- Sales Commissions: This is the variable compensation earned by a salesperson, typically calculated as a percentage of the revenue or profit they generate. It’s the primary incentive driving sales performance.

- Accrual Period: This is the specific timeframe—monthly, quarterly, or annually—over which commissions are calculated and recorded.

- Accrual Rate: The percentage or formula used to determine the commission amount. This can be a simple flat rate or a complex, multi-tiered structure.

- Accrual Method: The specific approach used to calculate the commission liability, which can range from simple to highly complex depending on the sales compensation plan.

Accounting for Accrued Commissions: The Journal Entries

Correctly recording accrued commissions involves a two-step process of journal entries: one to recognize the liability when it's earned, and another to clear it when the payment is made.

The critical moment for the initial entry is when the commission is considered earned. This trigger point must be clearly defined in your sales commission plan and can vary widely:

- Upon contract signature.

- When the customer is invoiced.

- Upon receipt of the first payment from the customer.

- When the service or product is delivered.

Once this trigger event occurs, the accounting team must record the expense and the corresponding liability.

Step 1: Recording the Accrual (When Earned)

Let's imagine it's the end of March. Your salesperson, Alex, has closed deals totaling $100,000 in revenue. According to their plan, they earn a 5% commission, which is paid out on the 15th of the following month (April).

In March, Alex has earned a commission of $5,000 (5% of $100,000). To reflect this in the March financial statements, you would make the following journal entry:

| Account | Debit | Credit |

|---|---|---|

| Commission Expense | $5,000 | |

| Accrued Commission Liability | $5,000 |

Impact on Financial Statements:

- Income Statement: The

Commission Expenseaccount is debited, increasing your expenses for March by $5,000 and reducing your net income for that period. - Balance Sheet: The

Accrued Commission Liabilityaccount is credited, increasing your current liabilities by $5,000. This shows the company owes this amount to its employee.

Step 2: Recording the Payment (When Paid)

On April 15th, when Alex receives the $5,000 commission payment through payroll, the liability is settled. The journal entry to reflect this cash outflow would be:

| Account | Debit | Credit |

|---|---|---|

| Accrued Commission Liability | $5,000 | |

| Cash | $5,000 |

Impact on Financial Statements:

- Balance Sheet: The

Accrued Commission Liabilityis debited, reducing the liability to zero. TheCashaccount is credited, reducing your company's cash balance by $5,000. - Income Statement: There is no impact on the April income statement because the expense was already recognized in March.

This two-step process ensures that your profitability for March is accurately stated, reflecting the true cost of sales for that month.

Why Automation is Crucial

Manually tracking earned dates, calculating commissions, and posting journal entries for every salesperson is time-consuming and prone to human error. Using a dedicated platform like Qobra automates these calculations by connecting directly to your CRM (like Salesforce or HubSpot). It provides finance and sales ops teams with reliable, auditable data, drastically reducing the time spent on month-end closing and eliminating the costly errors that often arise from complex spreadsheets.

Methods for Calculating Commission Accruals

The complexity of your commission accrual process depends entirely on the structure of your compensation plans. While some are straightforward, others require sophisticated calculation logic.

The Straightforward Approach: Percentage of Sales

This is the simplest method. A fixed percentage is applied to the total sales generated by a salesperson during the accrual period.

- Example: If the commission rate is 3% and a salesperson generates $80,000 in revenue, the accrued commission is simply

0.03 * $80,000 = $2,400.

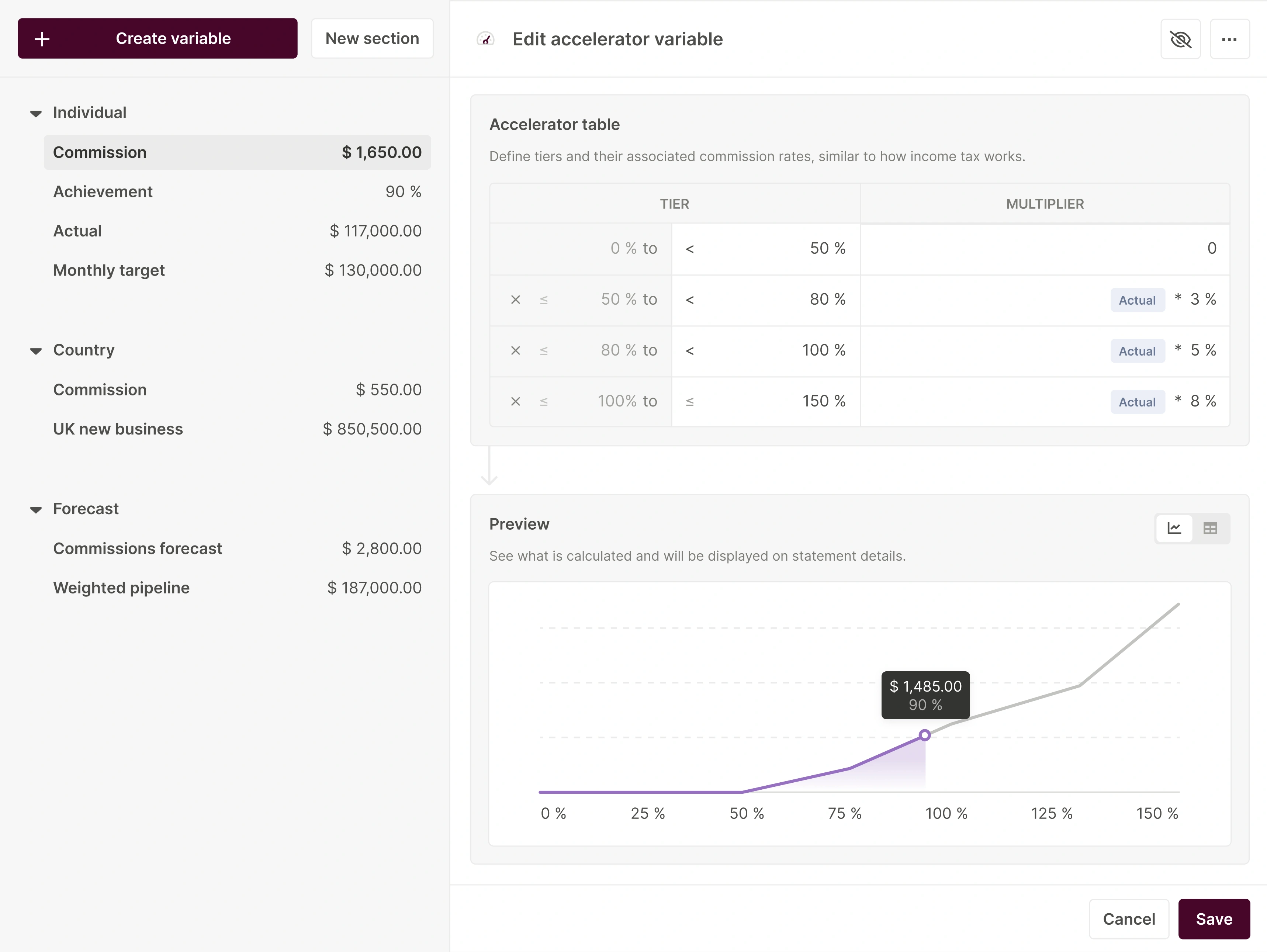

The Graduated Approach: Tiers and Thresholds

Many companies use a tiered structure to incentivize over-performance. The commission rate increases as a salesperson meets or exceeds certain sales targets or quotas.

- Example: A company offers 2% on the first $50,000 in sales, 4% on sales between $50,001 and $100,000, and 6% on sales above $100,000.

- A salesperson who generates $120,000 in revenue would earn:

($50,000 * 2%) = $1,000($50,000 * 4%) = $2,000($20,000 * 6%) = $1,200- Total Accrued Commission: $4,200

The Complex Approach: Multi-Variable Commissions

In many industries, especially B2B and SaaS, commissions are based on multiple factors beyond just revenue. These can include:

- Product type or service line (higher margins may carry higher commission rates).

- Contract length or deal terms.

- Gross profit margin of the deal.

- Customer retention or up-sell achievements.

- Team-based bonuses or "spiffs" for specific campaigns.

Calculating these commissions manually is not only a logistical nightmare but also a significant source of errors. This is where the power of an automated commission management platform becomes indispensable. Platforms like Qobra use a flexible, no-code rule editor that allows administrators to build and modify even the most complex plans without needing technical expertise, ensuring accuracy and saving dozens of hours each month.

Industry-Specific Accrual Scenarios

The timing and nature of commission accruals can vary significantly across different industries.

- SaaS (Software-as-a-Service): Commissions are often earned when a customer signs an annual contract (Annual Contract Value - ACV). The commission expense is typically recognized upfront, even if the customer pays in monthly installments. Some companies, following ASC 606 guidelines, may capitalize these costs and amortize them over the contract's life.

- Real Estate: The commission is clearly earned upon the successful closing of a property sale. The accrual would be recorded at the end of the month if the closing occurred, but the payout to the agent is scheduled for the following month. For more details, explore solutions for real estate commission tracking software.

- Insurance: An agent's commission is usually earned when a new policy is sold and the first premium is paid. Accruals would be made for policies sold near the end of an accounting period where payment is pending.

- Retail: Commissions are typically earned at the point of sale. Because payment often happens on a bi-weekly or monthly payroll cycle, any commissions earned between the last payroll run and the end of the month must be accrued.

Normative Differences: US GAAP (ASC 606) vs. IFRS 15

For many companies, especially in the US, accounting for commission costs has become more complex with the introduction of the ASC 606: Revenue from Contracts with Customers standard under US GAAP.

Under ASC 606, incremental costs of obtaining a contract—which directly includes sales commissions—must be capitalized as an asset if the company expects to recover those costs. This asset is then amortized (expensed) over a period that reflects the transfer of goods or services to the customer. This could be the contract term, or even an estimated customer lifetime if renewals are expected.

IFRS 15, the international equivalent, has similar principles, requiring costs to obtain a contract to be capitalized and amortized.

What does this mean in practice? Instead of expensing the entire commission in the period of the sale, you may need to:

- Record the commission cost as an asset (e.g., "Deferred Commission Costs").

- Systematically expense this asset over the life of the contract or the expected customer relationship.

This requirement adds another layer of complexity to tracking and accounting, making automated systems that can handle amortization schedules essential for compliance. You can learn more about managing commissions under ASC 606.

Transparency Drives Motivation

Beyond accounting accuracy, transparent commission tracking is a powerful motivational tool. When salespeople have real-time visibility into their earned and potential commissions, they are more engaged, driven, and confident in their compensation plan. Platforms like Qobra provide personalized dashboards for each rep, showing exactly how their performance translates into earnings, which helps eliminate disputes and keeps the team focused on hitting their targets.

Mastering accrued commissions is more than a finance function; it's a strategic imperative. It ensures regulatory compliance, provides leadership with a true view of profitability, and builds trust with your sales team. By moving beyond manual processes and embracing automation, you can transform a complex administrative burden into a streamlined system that supports growth and motivates your most critical revenue-generating teams.

FAQ: Accrued Commissions

What is the difference between "accrued commissions" and "commissions payable"?

While often used interchangeably, there can be a subtle distinction. "Accrued commissions" refers to the liability built up over an accounting period through an adjusting entry at month-end. "Commissions payable" can sometimes refer to the specific amount that has been finalized and is officially due for payment in the next payroll cycle. In practice, many companies use a single account, "Commissions Payable" or "Accrued Liabilities," to record this obligation.

How do accrued commissions affect a company's financial statements?

Accrued commissions have a dual impact. On the income statement, they are recognized as a "Commission Expense," which reduces the company's net income for the period. On the balance sheet, they are recorded as a current liability (under "Accrued Commission Liability" or similar), which increases the total amount the company owes. This ensures both statements reflect the company's financial position and performance accurately.

Can you reverse an accrued commission?

Yes, an accrual can and should be reversed if the underlying condition for the commission is no longer met. A common example is a "clawback" situation where a customer cancels their contract shortly after signing, and the commission plan stipulates that the commission must be returned. In this case, a reversing journal entry would be made to debit the liability account and credit the expense account, effectively removing the previously recorded commission.

How does software help manage commission accruals?

Commission management software like Qobra automates the entire process. It integrates with your CRM to pull in real-time sales data, applies complex commission rules automatically, and generates precise accrual reports for the finance team with just a few clicks. This eliminates manual errors, saves dozens of hours of administrative work, ensures compliance with standards like ASC 606, and provides complete transparency for the sales team through interactive dashboards. It transforms the process from a reactive, error-prone task to a proactive, strategic advantage.